Analyze

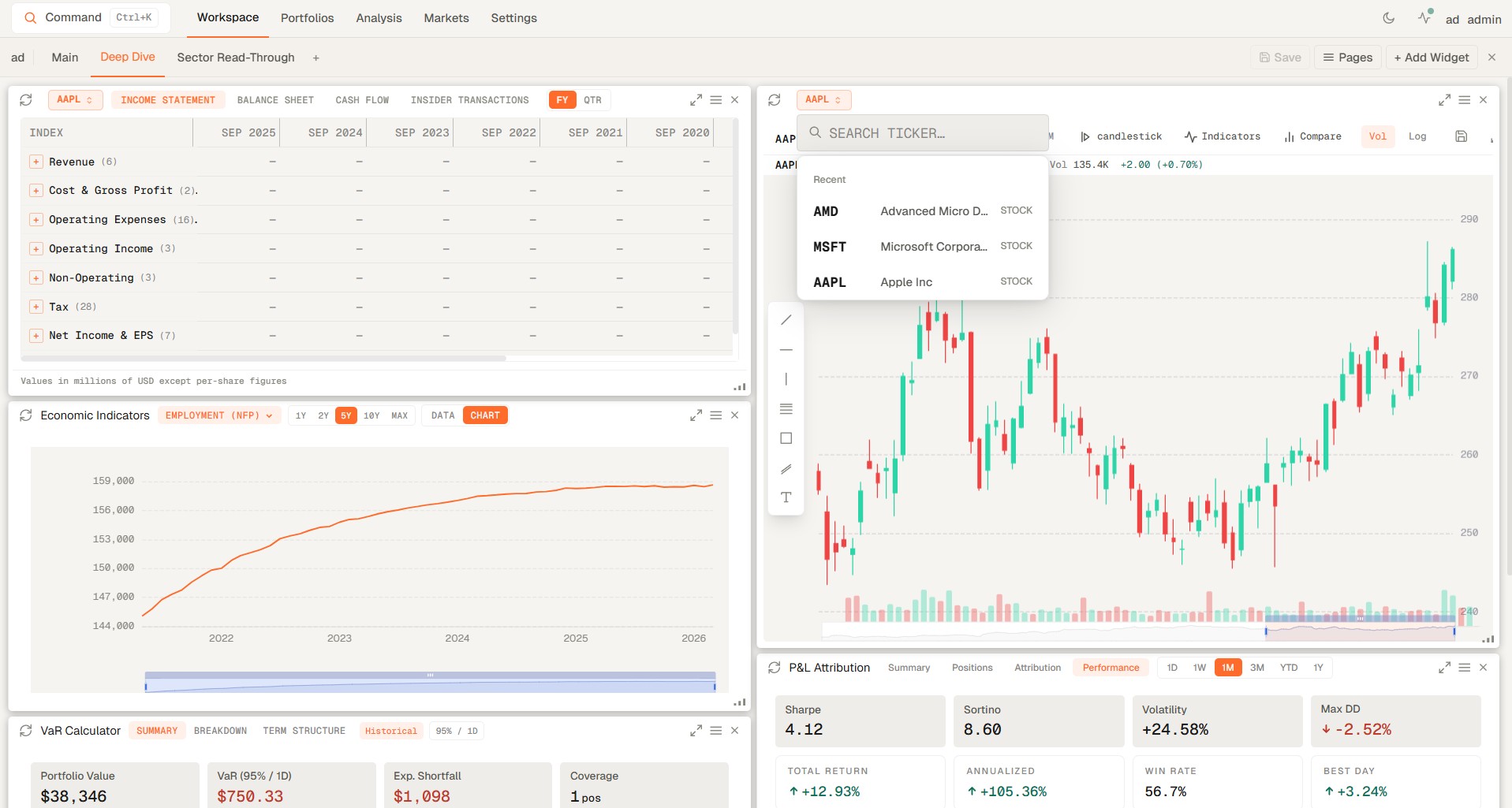

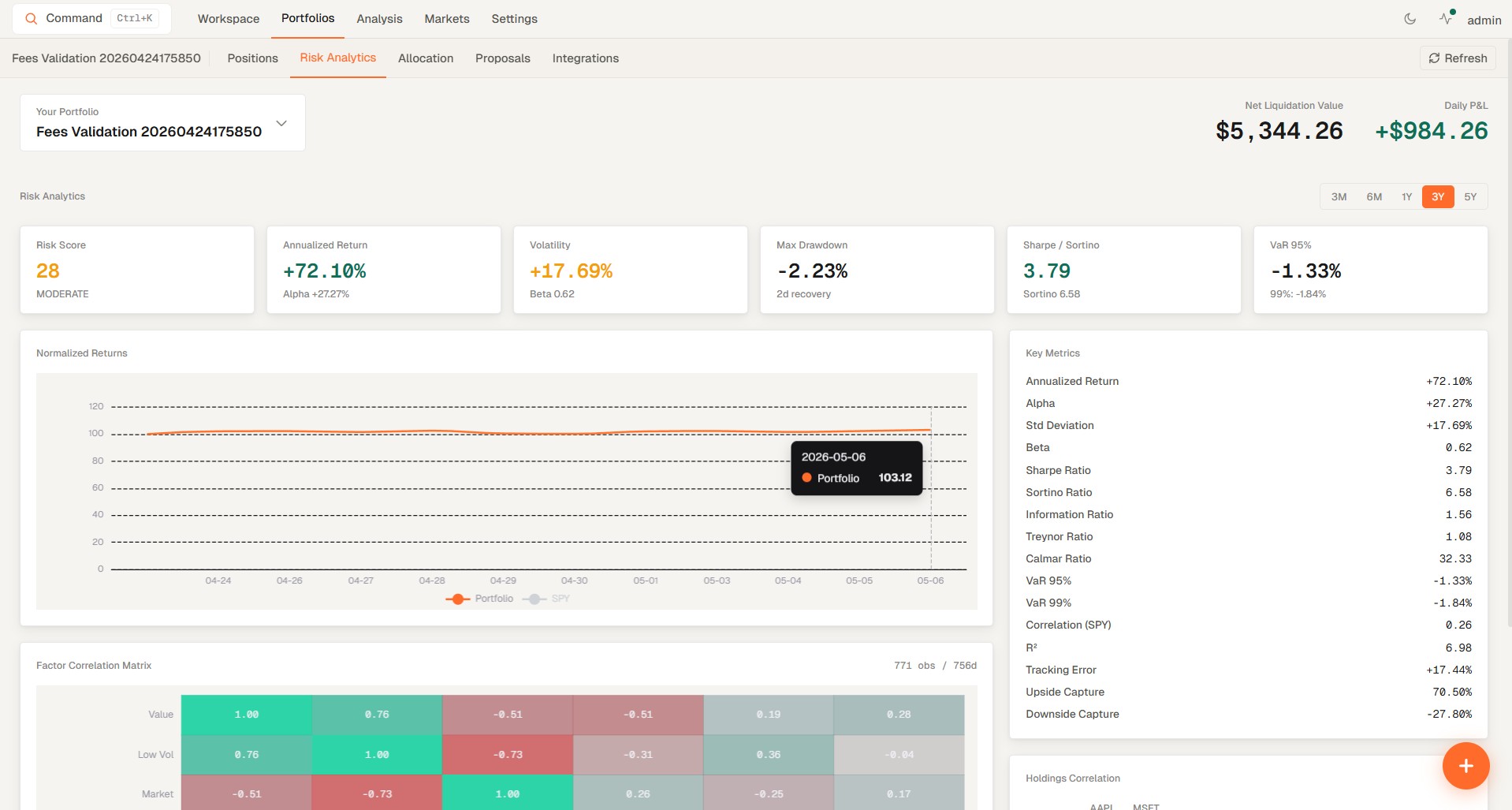

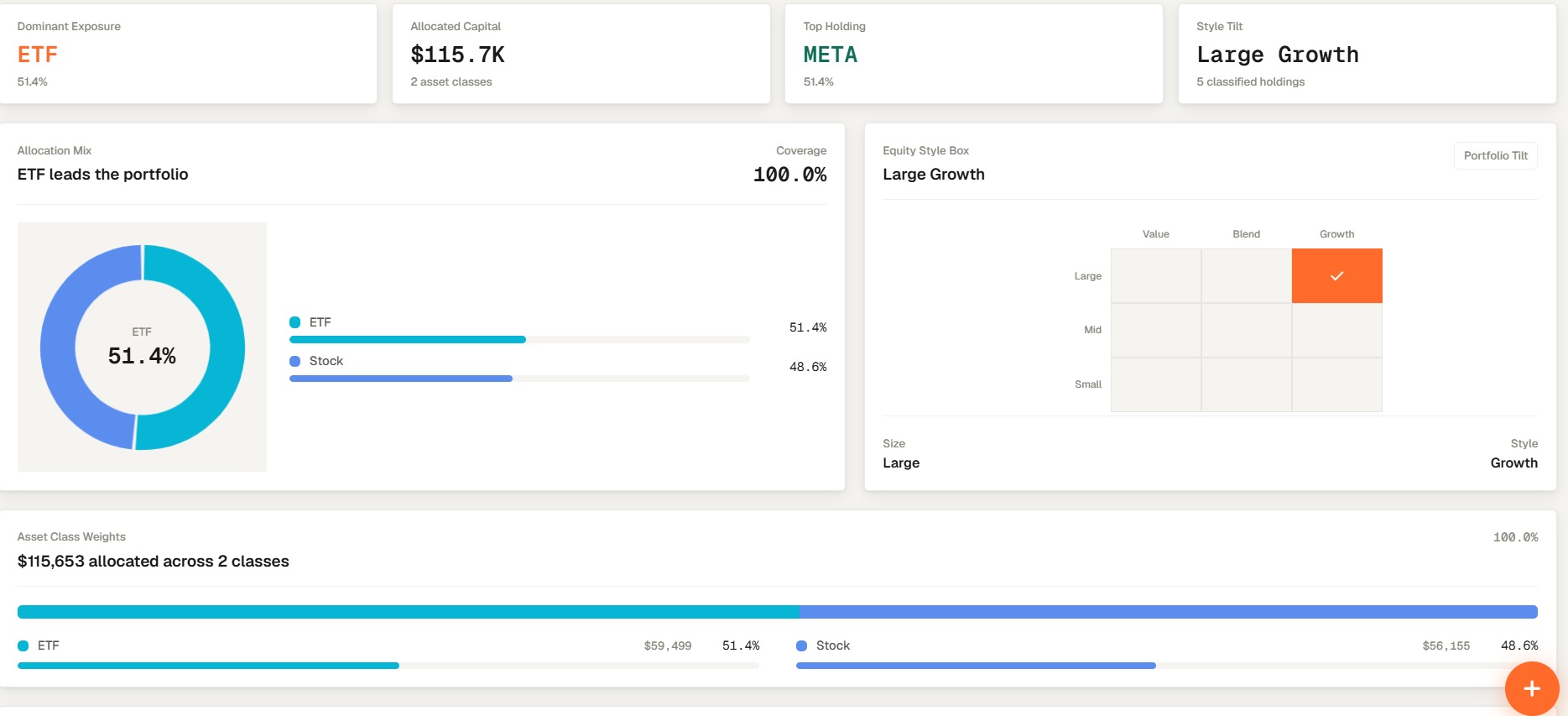

Understand portfolio risk, allocation, exposures, concentration, and historical behaviour.

Portfolio risk analytics & proposal software

Portfolio risk analytics and proposal software built for independent financial advisors and RIAs. Analyze client and prospect portfolios, uncover the risks that matter, compare portfolios with your models, and turn your analysis into fully editable proposals.

One connected advisor workflow

Portfolio analysis should lead somewhere. Genesis connects the steps between understanding a portfolio and presenting your analysis—so you can move from a client or prospect portfolio to a professional proposal without rebuilding your work across disconnected tools.

Understand portfolio risk, allocation, exposures, concentration, and historical behaviour.

Compare existing portfolios with your models and see how risk, allocation, exposure, and performance differ.

Turn your analysis into a fully editable proposal built around the client conversation.

Analyze. Compare. Propose.

A portfolio can appear diversified while still carrying concentrated, correlated, or hidden exposures. Genesis gives financial advisors and RIAs a deeper view of portfolio risk—helping you understand what is actually shaping portfolio behaviour beyond holdings and headline performance.

Turn complex portfolio analytics into clearer insights for the conversations that matter.

Your models represent how you think portfolios should be constructed. Genesis brings that investment approach directly into the analysis.

Create and manage model portfolios, define target allocations, backtest strategies, and compare client or prospect portfolios against your models. Make the comparison clear before the conversation begins.

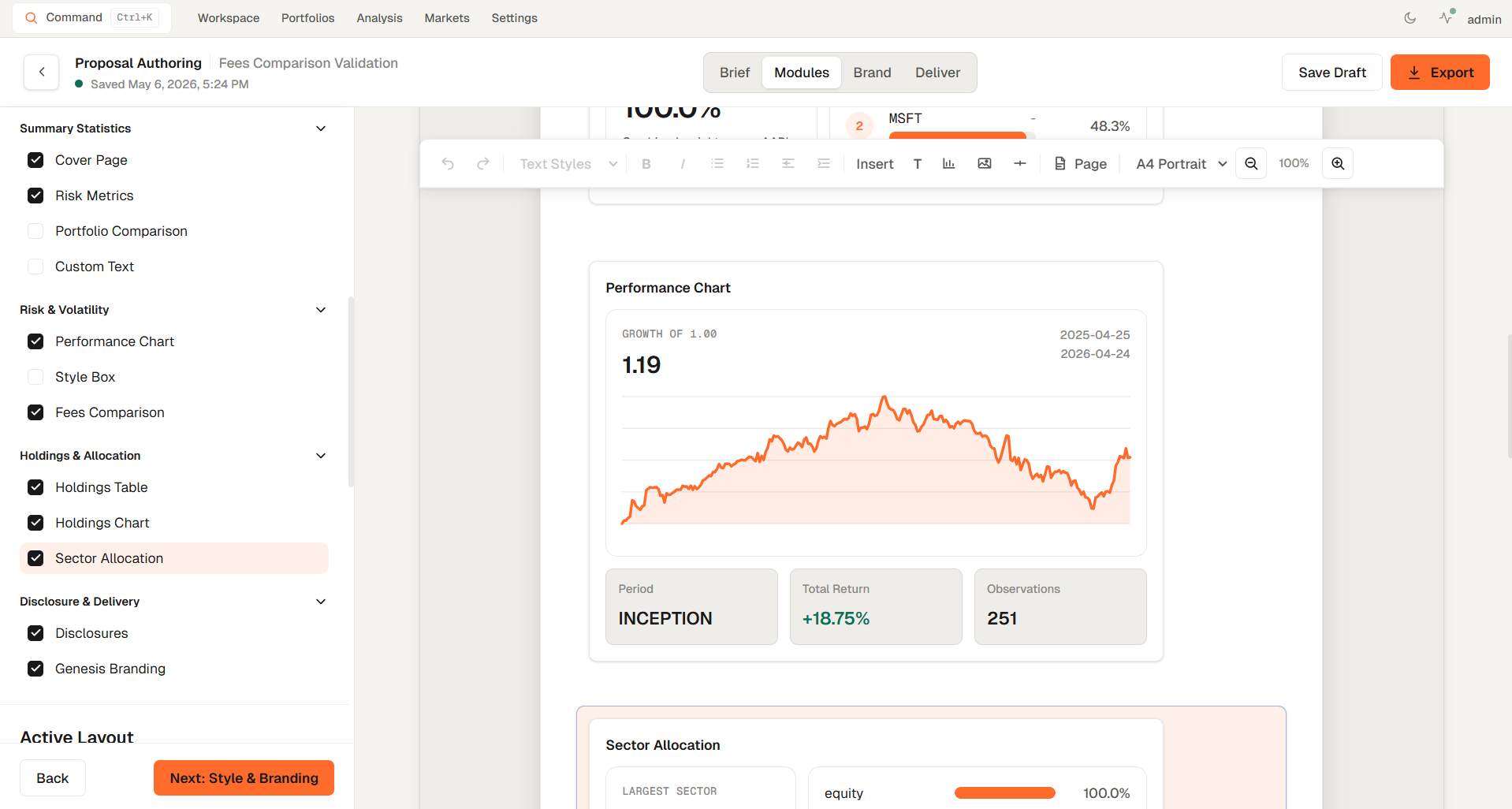

The analysis is already done. You should not have to rebuild it somewhere else. Genesis lets you move directly from portfolio analytics and model comparisons into a professional, client-ready proposal.

Customize the narrative, add your own content, and restructure the document around the conversation. Then export the finished proposal to Word or PDF.

Why Genesis

Finding an insight is only the beginning. Genesis connects portfolio analysis to what comes next—understand the portfolio, compare it with your investment approach, and turn the analysis into something you can actually use in the client conversation. Instead of moving between analytics tools, spreadsheets, presentations, and document editors, Genesis brings the workflow together.

See the risks, exposures, and behaviour that matter.

Understand how the portfolio differs from your models.

Turn the work into a fully editable proposal.

Built for advice

Genesis is built for independent financial advisors and RIAs that want deeper portfolio analytics without adding more disconnected steps to their process.

Portfolio risk analytics, model comparison, client organization, and proposal creation—connected around the way advisors actually work.

See Genesis for Financial AdvisorsUnderstand what a prospect actually holds before the first proposal.

Uncover risks that may not be visible from holdings alone.

Create and manage the models that represent your investment approach.

See how existing portfolios differ from your models across risk, allocation, and exposure.

Turn the analysis into a professional proposal without leaving the platform.

FAQ

These are the questions independent financial advisors and RIAs usually ask before moving portfolio analysis, model comparison, and proposal creation into one connected workflow.

Genesis Risk Monitor is portfolio risk analytics and proposal software built for independent financial advisors, RIAs, and wealth management professionals who want deeper portfolio analysis connected directly to client-ready proposals.

Analyze means understanding portfolio risk, allocation, exposures, concentration, and historical behaviour. Compare means reviewing client or prospect portfolios against your own model portfolios. Propose means turning that analysis into a fully editable client proposal without rebuilding the work in another tool.

Genesis measures portfolio risk with metrics including Value at Risk, Expected Shortfall, volatility, beta, Sharpe ratio, and maximum drawdown, alongside concentration, sector, country, currency, and factor exposure analysis, scenario analysis and stress testing, correlation insights, and portfolio backtesting.

Yes. You can create and manage model portfolios, define target allocations, backtest strategies, and compare existing client or prospect portfolios against your models across risk, allocation, exposure, and performance.

Yes. Proposals in Genesis are fully editable documents rather than fixed report templates. You can bring portfolio data, charts, and analytics into the document, customize the narrative and structure, and export the finished proposal to Word or PDF.

No. Genesis Risk Monitor provides calculations, visualizations, and structured workflows. Users remain responsible for reviewing data quality, assumptions, interpretation, and the decisions taken from the analysis.

Get started

See the portfolio more clearly. Compare the alternatives. Present your analysis with confidence. Bring portfolio risk analytics, model portfolios, and proposal creation into one connected workflow built for financial advisors and RIAs.

Start your free trial and see how Genesis fits your workflow.